This article provides a range of insights into the complexities of Social Security and Medicare, focusing on when and how to enroll, strategies to maximize benefits, and the potential future challenges of these programs. It discusses key concepts such as the “Older Spouse Strategy” and the “Higher-Earner Deferral Strategy” for optimizing Social Security benefits. Additionally, it highlights the importance of considering individual circumstances and financial needs when making enrollment decisions. The article also addresses Medicare, including enrollment periods and the importance of understanding healthcare coverage options. It emphasizes the significance of income-related factors in determining Medicare costs and the need for financial planning in retirement.

- Social Security is a government agency established in 1935 to provide income to retired workers, aiming to promote economic security. Eligibility for Social Security benefits is based on work records, requiring ten or more years of work and Social Security tax contributions.

- The age to start receiving Social Security benefits varies, with early initiation at 62 resulting in reduced payments, and delaying benefits until 70 increases them.

- Strategies to maximize Social Security benefits include the “Older Spouse Strategy” and the “Higher-Earner Deferral” strategy, considering factors like financial needs and longevity.

- Medicare is a government-provided health insurance program for individuals aged 65 and older, with enrollment periods based on various factors. The annual open enrollment period allows beneficiaries to make changes to their Medicare coverage. Medicare has different parts, and beneficiaries can make changes during open enrollment from October 15 to December 7th.

Costs for Medicare vary, including Part A and Part B premiums, with income-related adjustments and considerations for supplemental plans and prescription drug plans. High-income individuals may face increased Medicare premiums due to the Income-Related Monthly Adjustment Amount (IRMAA).

A few years ago, my mother called me, saying “I am turning 62 – how do I apply for Medicare?” I quickly and politely explained that at age 62, you can enroll early into Social Security, but Medicare will kick in at age 65. Needless to say, she realized retirement may need to wait for three more years and was grateful someone could help her understand the differences between the two systems. This conversation and confusion is common among the Baby Boomers heading into this phase of their lives.

As you will read below, 62, 65, 66.7 and 70 are ages used in relation to Social Security and Medicare.

In this article, we will explain when someone can enroll in Social Security and Medicare coverage and summarize the differences between each system. As you approach these milestones, it can be daunting from an emotional standpoint as you transition into the next phase of your life and from a financial standpoint, as these enrollments and elections can significantly impact your post-retirement needs.

What is Social Security and who is eligible for benefits?

Social Security is a governmental agency that provides retired workers a continuing income after retirement. It was signed into law in 1935 as part of the New Deal and the goal was to promote the economic Security of the nation’s people. What-is-Social-Security.pdf

You can be eligible for benefits on your work record if you worked and paid Social Security taxes for ten years or more. Or you can qualify for benefits based on your current or former spouse’s work record. Plus, your children may be eligible for a benefit if they are under age 18, age 18 or 19 and attend elementary or high school full time or are of any age and have a disability. (Source: https://www.ssa.gov/retirement/eligibility

When can someone start receiving benefits?

Initiating benefits can occur between ages 62 and 70. Starting early reduces benefits but allows for a longer accumulation period while delaying increases benefits but shortens the accumulation phase. Below are some considerations for when to start enrollment:

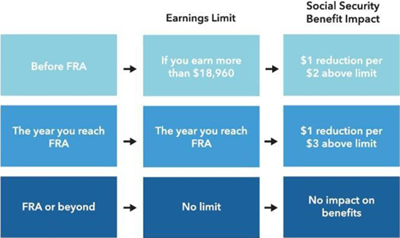

- Claiming Early: Initiating benefits at 62 results in a roughly 30% reduction in monthly payments compared to waiting for full retirement age (66 or 67, depending on the birth year). Note that if you continue to work between the ages of 62 and full retirement age (“FRA”), your benefits will be reduced even further. The benefit is reduced by $1 for each $2 you earn above the annual limit (in 2023, the limit is $21,240). How-Work-Affects-Your-Benefits.pdf

- Delaying Benefits: Each year delayed after full retirement age until 70 increases benefits by 8%. This offers a hedge against longevity risk and can be a significant upside for those with a longer life expectancy.

Everyone’s situation is different and will require understanding various factors when choosing the age to enroll. The factors include but are not limited to health and life expectancy, financial needs, and other sources of retirement income.

What are strategies to maximize benefits?

The Older Spouse Strategy

One of the key decisions that individuals face when planning for retirement is when to claim their Social Security benefits. This decision becomes even more crucial for married couples, as it can significantly impact their overall retirement income. One strategy that is often recommended in certain situations is the “Older Spouse Strategy.” This strategy involves the older spouse waiting until age 70 to claim their Social Security benefits to maximize the benefits available to the younger spouse after the older spouse’s demise.

Let’s consider an example to understand how the “Older Spouse Strategy” works. Suppose John is 65 years old and his wife, Sarah, is 60 years old. John has a higher earning history and is eligible for a higher Social Security benefit. If John were to claim his benefits at 65, he would receive a reduced benefit amount. However, John will receive the maximum benefit if he waits until he is 70 to claim his benefits.

Now, let’s fast forward to the unfortunate event of John’s demise. As a surviving spouse, Sarah would be eligible to receive survivor benefits based on John’s earnings record. The survivor benefit is equal to the amount that John received at the time of his death, or the maximum benefit amount he would have received at 70. By waiting until 70 to claim his benefits, John has effectively increased the survivor benefit that Sarah will receive.

The Older Spouse Strategy offers several advantages for married couples. Here are some key benefits:

- Maximizing benefits: By delaying the older spouse’s claim until 70, the couple can maximize their overall Social Security benefits. This can provide them with a higher income during their retirement years.

- Protecting the surviving spouse: The strategy ensures that the surviving spouse, who is typically younger, can receive a higher survivor benefit for a longer duration. This can be particularly beneficial if the surviving spouse has a longer life expectancy.

- Increasing financial Security: By maximizing their Social Security benefits, couples can enhance their financial Security in retirement. The higher benefits can help cover essential expenses and provide a buffer against unexpected costs.

The Older Spouse Strategy can be a valuable approach for married couples looking to maximize their Social Security benefits and provide financial Security for the surviving spouse. By waiting until age 70 to claim benefits, the older spouse can ensure that the younger spouse receives a higher survivor benefit in the event of their demise. However, carefully evaluating individual circumstances and seeking professional advice before implementing this strategy is crucial. Making an informed decision can help couples optimize their retirement income and achieve their financial goals.

Higher-Earner Deferral strategy

The “Higher-Earner Deferral” strategy is based on the fact that delaying Social Security benefits beyond the full retirement age can increase monthly benefits. Each year benefits are delayed, the monthly benefit amount can increase by a certain percentage, known as the Delayed Retirement Credits (DRCs). Waiting until age 70 can increase your benefits by up to 32%.

In the context of couples, the Higher-Earner Deferral strategy focuses on the higher-earning spouse delaying their benefits until age 70, while the lower-earning spouse claims their benefits at their full retirement age, or even earlier if necessary. By deferring the benefits of the higher-earning spouse, the couple can ensure that the surviving spouse will receive the highest possible benefit amount in the event of the higher-earning spouse’s passing.

Advantages of the Higher-Earner Deferral Strategy:

- Maximizing Lifetime Benefits – By deferring benefits until age 70, the higher-earning spouse can significantly increase their monthly benefits. This can result in a higher total payout over their lifetime, especially if they have a longer life expectancy. The surviving spouse can then claim the higher benefit amount, providing a more substantial income stream throughout their retirement.

- Protecting the Surviving Spouse – The Higher-Earner Deferral strategy protects the surviving spouse’s financial well-being. Since the surviving spouse is entitled to the higher of the two benefit amounts, by maximizing the benefits of the higher-earning spouse, the surviving spouse can receive a larger benefit, potentially providing them greater financial Security.

- Tax Planning Opportunities – Delaying Social Security benefits can also have tax planning benefits. By deferring benefits until age 70, retirees may have a lower taxable income during earlier retirement years. This can lower tax liabilities and enable couples to use other tax-saving strategies.

While the Higher-Earner Deferral strategy can be advantageous, there are several considerations and limitations to consider.

- Financial Needs and Longevity – Before implementing this strategy, it is important to assess your financial needs and consider your life expectancy. If the higher-earning spouse has a shorter life expectancy or the couple requires the additional income earlier, claiming benefits earlier may be more beneficial.

- Delayed Retirement Credits Stop at Age 70 – It’s important to note that delayed retirement credits stop accumulating once you reach age 70. Therefore, there is no financial advantage to delaying benefits beyond this age. If the higher-earning spouse has already reached age 70, there may be other options than employing this strategy.

- Individual Circumstances – Each couple’s financial situation is unique, and the Higher-Earner Deferral strategy may not be the best approach for everyone. Factors such as other sources of income, health conditions, and financial goals should be taken into account when determining the optimal Social Security claiming strategy.

The Higher-Earner Deferral strategy is a powerful approach couples can utilize to maximize their Social Security benefits. By deferring benefits until age 70 for the higher-earning spouse, couples can ensure a higher monthly benefit for the surviving spouse and potentially increase their total lifetime benefits. However, it’s crucial to carefully evaluate individual circumstances before making a decision.

What does the future hold for Social Security?

The potential depletion of the Social Security Trust Fund by 2033 highlights the importance of strategic planning when it comes to Social Security benefits. Individuals and couples must carefully consider various factors, especially considering the possibility of benefit reductions. A recent analysis indicates that, without policy adjustments, a typical newly retired dual-income couple could face an annual reduction in benefits of approximately $17,400 by 2033. While legislative measures can alter the trajectory of the Trust Fund’s solvency, adopting a conservative approach and planning for uncertainties is a prudent course of action.

What is Medicare?

Medicare is a government-provided health insurance program that offers coverage to individuals who are 65 years or older. It is designed to help older adults and certain individuals with disabilities access medical services and reduce the financial burden of healthcare expenses. While Medicare provides essential coverage, it is important to understand the factors that can influence the cost of premiums and the availability of supplemental coverage.

It is important for individuals considering Medicare to research and compare the available plans and supplemental coverages in their county. This can help them understand the premiums associated with different options and choose a plan that best suits their healthcare needs and budget. The Medicare website (medicare.gov) provides tools and resources to help individuals navigate the available options and make informed decisions.

When can you enroll in Medicare?

Enrollment in Medicare can commence three months prior to your 65th birthday, during the month of your 65th birthday, and continues for three months following your 65th birthday. Failure to enroll during this period, and if you lack coverage through an employer, may result in a lifelong late enrollment penalty applied to your premiums. If you continue working past the age of 65 for an employer with more than 20 employees, you have the option to delay signing up for Medicare Part B (more details on Medicare parts will be provided later). Your employer-provided insurance becomes the primary payer, with Medicare as the secondary payer. However, if your employer has fewer than 20 employees, you may need to enroll in both Parts A and B when you turn 65, with Medicare as the primary payer. Different rules apply to those who are self-employed or have Medicaid or Marketplace insurance. In such cases, it is advisable to seek guidance from a qualified expert.

Source: https://www.medicare.gov/basics/get-started-with-medicare/medicare-basics/working-past-65

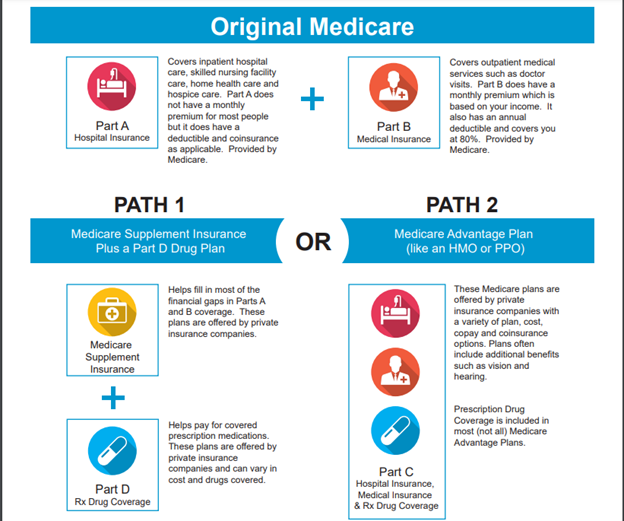

What are the “Parts” of Medicare?

Once you enroll in Original Medicare or a Medicare Advantage Plan, you have the opportunity to join, drop, or switch to another plan annually during the open enrollment period. Open enrollment commences on October 15 and concludes on December 7. This period provides beneficiaries with the chance to make adjustments to their Medicare coverage to better align with their healthcare needs.

Medicare_Inforgraphic_Choosing-your-own-path.pdf

During the open enrollment period, if you initially enrolled in Original Medicare, you have the option to switch to a Medicare Advantage Plan. However, if you are already enrolled in a Medicare Advantage Plan and wish to return to Original Medicare with Supplemental plans, this change can only be made during the Medicare Advantage Open Enrollment period, which runs from January 1 to March 31. It’s essential for beneficiaries to be aware of these enrollment periods to make informed decisions about their Medicare coverage.

Source: https://www.medicare.gov/basics/get-started-with-medicare/get-more-coverage/joining-a-plan

When enrolling in Original Medicare plans with supplemental coverage, it’s crucial to have answers to the following questions to make informed choices about your healthcare coverage:

- What hospital system do you use? Understanding which hospital systems are in-network or preferred can help you access the healthcare facilities that best suit your needs.

- Do you have a preferred provider? If you have specific healthcare providers you prefer to see, knowing if they are part of the plan’s network is important to ensure continuity of care.

- Will you need coverage in multiple states? If you travel frequently or split your time between different states, you should consider coverage options that provide benefits in multiple locations.

- What prescriptions do you take? How are they delivered? Listing your current prescriptions and understanding how they are covered, including copayments or mail-order options, can help you choose a plan that meets your medication needs.

Having answers to these questions can guide you in selecting the most suitable Medicare plan and supplemental coverage for your unique healthcare requirements.

The costs for Medicare can vary depending on individual circumstances. Here’s an overview of the typical costs associated with Medicare:

Medicare Part A:

- For those who qualify for “Premium-free Part A” (usually based on work history), there is no monthly premium.

- If you don’t qualify for premium-free Part A, the monthly premium can be either $278 or $506 in 2023, depending on your work history and Medicare tax payments.

Medicare Part B:

- The standard monthly premium for Medicare Part B in 2023 is $164.90 per month.

- However, some individuals may pay higher premiums based on their income through the Income-Related Monthly Adjustment Amount (IRMAA). The IRMAA affects individuals with higher incomes.

It’s important to note that while Part A covers hospital services and Part B covers medical services and doctor visits, they do not cover all healthcare expenses. Many individuals also choose to enroll in additional coverage, such as Medicare Advantage Plans (Part C) and Medicare Prescription Drug Plans (Part D), which come with their own premiums and costs.

Supplemental plans like Parts G and F, as well as Part D plans, can have premiums that vary depending on the insurance carrier and your individual prescription drug needs. To get accurate quotes for these plans tailored to your specific circumstances, it’s advisable to consult with a Medicare expert.

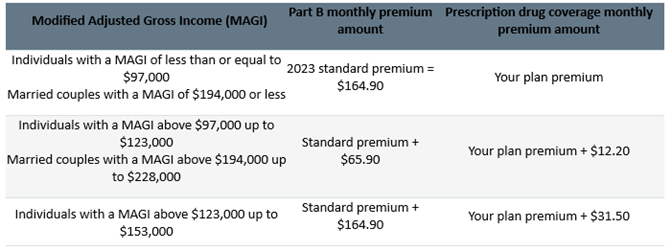

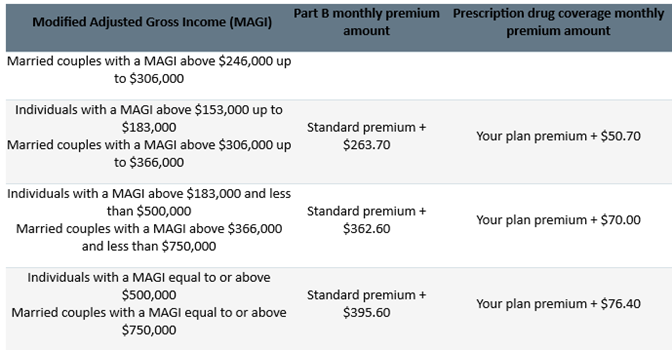

Additionally, it’s essential for high-income taxpayers to be aware of the Income-Related Monthly Adjustment Amount (IRMAA) mentioned earlier. IRMAA can result in higher Medicare Part B and Part D premiums if your income exceeds certain thresholds. Staying informed about these adjustments and planning accordingly is crucial for individuals with higher incomes.

It’s also important to be aware of the income thresholds that can trigger higher premiums for Medicare Part B and prescription drug coverage. These thresholds can significantly impact your annual healthcare costs, so understanding where you fall in terms of income is essential for financial planning in retirement.

For those who file income taxes as “married, filing jointly” with a total adjusted gross income plus tax-exempt interest income of $194,000 or more, or for individuals who file individual tax returns or joint tax returns as a married couple, the specific income-related monthly adjustment amounts (IRMAA) mentioned in the chart will apply. These IRMAA amounts can lead to higher Medicare premiums, so individuals falling into these income categories should be prepared for potential increases in their healthcare expenses. Proper financial planning can help individuals optimize their retirement finances and ensure they are prepared for potential premium increases based on their income.

If you’re single and filed an individual tax return, or married and filed a joint tax return, the following chart applies to you:

https://www.ssa.gov/benefits/medicare/medicare-premiums.html

https://www.ssa.gov/benefits/medicare/medicare-premiums.html

Author: Katie Madzsar, CFP®, AEP®, Senior Wealth Advisor, Managing Director, Wellspring Financial Advisors, LLC

Information as of September 20, 2023

Any suggestions contained herein are general, and do not take into account an individual’s or entity’s specific circumstances or applicable governing law, which may vary from jurisdiction to jurisdiction and be subject to change. Distribution hereof does not constitute legal, tax, accounting, investment, or other professional advice. Recipients should consult their professional advisors prior to acting on the information set forth herein.

Navigating the Crossroads of Retirement